Multiple Reporting Currencies Overview

Multiple Reporting Currencies (MRC) is a set of unique features imbedded in Oracle Applications that permits an organization to report in multiple functional currencies. Using MRC, you can maintain and report accounting records at the transaction level in more than one functional currency. You do this by defining one or more reporting sets of books, each associated with a primary set of books. Each set of books has its own functional currency. The following Oracle Applications support Multiple Reporting Currencies:

a) General Ledger

b) Payables

c) Purchasing

d) Receivables

e) Cash Management

f) Projects

g) Assets

h) Cost Management

i) Global Accounting Engine

Use of MRC:

MRC is intended for use by organizations that must regularly and routinely support statutory and legal reporting of both transactions andGeneral Ledger account balances in multiple currencies, other than the primary functional currency. If you only need to report balances in a currency other than your primary functional currency, you can use General Ledger translation.

MRC Features

a) Transaction–Level Conversion

When you enter transactions in Oracle Applications that support MRC, they are automatically converted into your primary functional currency and each of your reporting functional currencies, in accordance with the following:

- Primary functional currency transactions: All transactions denominated in your primary functional currency are recorded in this currency. The transactions are also converted automatically into each of your reporting functional currencies.

- Foreign currency transactions: Transactions denominated in a foreign currency are automatically converted into your primary functional currency and into each of your reporting functional currencies as wellunless the foreign currency matches the reporting functional currency (conversion not required).

When you enter transactions into Oracle Applications subledgers that support MRC, the transactions are converted into your primary and reporting functional currencies at the time of original entry. The primary functional currency amounts and their associated reporting currency amounts are stored together in your subledgers. You must post subledger transactions to General Ledger in the primary set of books and in each reporting set of books.

c) Inquiry and Reporting in Multiple Currencies

Because subledger transactions are converted into your reporting functional currencies at the time of original entry, the converted transactions are available for immediate inquiry and reporting.

After you have posted your subledger transactions to General Ledger in the primary set of books and in each associated reporting set of books, you can log into a General Ledger reporting responsibility, post the newly created journals, and report the journals and the account balances of the reporting set of books. When you inquire on account balances and journals in a reporting set of books, you can drill down to the subledger details (in your reporting functional currency), using General Ledger’s integrated drilldown features to provide complete and consistent views of underlying subledger transactions.

You can drill down from General Ledger to transaction details within Oracle Receivables, Oracle Payables, Oracle Projects, Oracle Assets, Oracle Purchasing, Oracle Inventory, and Oracle Work in Process.

Processes

There are three key processes in Oracle General Ledger to address multi-currency requirements:

1. Conversion: refers to foreign currency transactions that are immediately converted at the time of entry to the ledger's currency in which the transaction takes place.

2. Revaluation: adjusts asset or liability accounts that may be materially understated or overstated due to a significant fluctuation in the exchange rate between the time the transaction was entered and the time revaluation takes place.

3.1. Translation: restates an entire ledger or balances for a company from the ledger currency to another currency. The cumulative translation adjustment is typically recorded as part of equity.

3.2 Remeasurement: restates an entire ledger or balances for a company from the ledger currency to another currency. For non-monetary items, remeasurement uses historical rates. The cumulative translation adjustment is typically recorded as part of profit or loss.

To use multi–currency accounting, you must first define Currencies and Conversion Rate Types. Currency processes perform revaluation, translation, and remeasurement using daily or historical rates that you enter. Daily rates can be entered manually, using a spreadsheet interface or loaded in the GL_DAILY_RATES_INTERFACE table using SQL instructions.

Translation vs. Remeasurement

General Ledger performs translation in compliance with multiple national accounting standards, in particular SFAS #52 and IAS 21. General Ledger can perform two types of translation stipulated in SFAS #52 and IAS 21:

1. Translation or Equity Translation Method

2. Remeasurement or Temporal Method Translation

The translation method you use depends on your ledger currency (as discussed in SFAS #52 and IAS 21):

1. If the accounting ledger currency (as discussed in SFAS #52 and IAS 21) is different from the currency assigned to the ledger, books of record must be remeasured into the ledger currency before being translated into the reporting currency. If the ledger currency (as discussed in SFAS #52 and IAS 21 is the reporting currency, remeasurement

eliminates the need for translation.

2. If the accounting ledger currency (as discussed in SFAS #52 and IAS 21) is the same as the currency assigned to the ledger, books of record can be directly translated into the reporting currency without remeasurement.

The example and table, below, illustrates when translation and remeasurement are required.

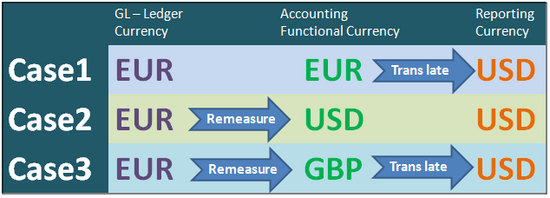

Consider U.S. company A has a wholly owned subsidiary, company B, that operates in Europe. The reporting currency is USD. The translation–remeasurement possibilities for company B are listed horizontally by case examples in the following diagram:

In Case 1, Company B's accounting ledger currency and ledger currency are the same. Company B's

ledger currency is not the same as the parent's functional or reporting currency.

However, this usually arises when the subsidiary is not integral to the parent's business.

In order to meet the reporting requirements of the parent, Company B has to perform translation from EUR to USD.

In Case 2, Company B's accounting ledger currency is different from its ledger currency. However, Company B's accounting ledger currency is the same as the parent's functional or reporting currency. This usually arises when the subsidiary is integral to the parent's business and cannot be sold without a severe impact to the parent. Company B remeasures its accounts from EUR to USD, which is also the reporting currency. In this case, remeasurement into the reporting currency eliminates the need for translation.

In Case 3, Company B's accounting ledger currency is GBP. Company B's accounting ledger currency is neither

its ledger currency nor the reporting currency. This is a rare case and could arise if the subsidiary is a holding company for operations in England. In this case, both remeasurement and translation are required. Company B first remeasures its accounts from EUR to GBP, then translates the accounts from GBP to USD.

Ok here is the differenece

Ok here is the differenece

In Financial standards (IAS 21 and FAS 52), Functional Currency is a test for the integration of your overseas and home businesses. If the businesses share a Functional currency, they are integrated, and you must use a financial statement conversion method called “remeasurement”. If the businesses do not share a Functional Currency, they are stand alone, and you must use a financial statement conversion method called “translation”. To determine the Functional currency, there are a series of cash flow related tests: it is an objective, situational determination, and not an optional choice.

Now just because your auditors tell you that your functional currency is Euro, this does not mean that you need to go about the tricky business of changing your Ledger Accounting Currency (or Set of Books functional currency) to Euro. What it means is that you need to remeasure in Euro rather than translate.

To do this re measurement you can use

1. The GL translation program

2. A secondary Ledger

you can read the complete article @

http://davidhaimes.wordpress.com/2008/06/26/what-is-your-functional-currency/